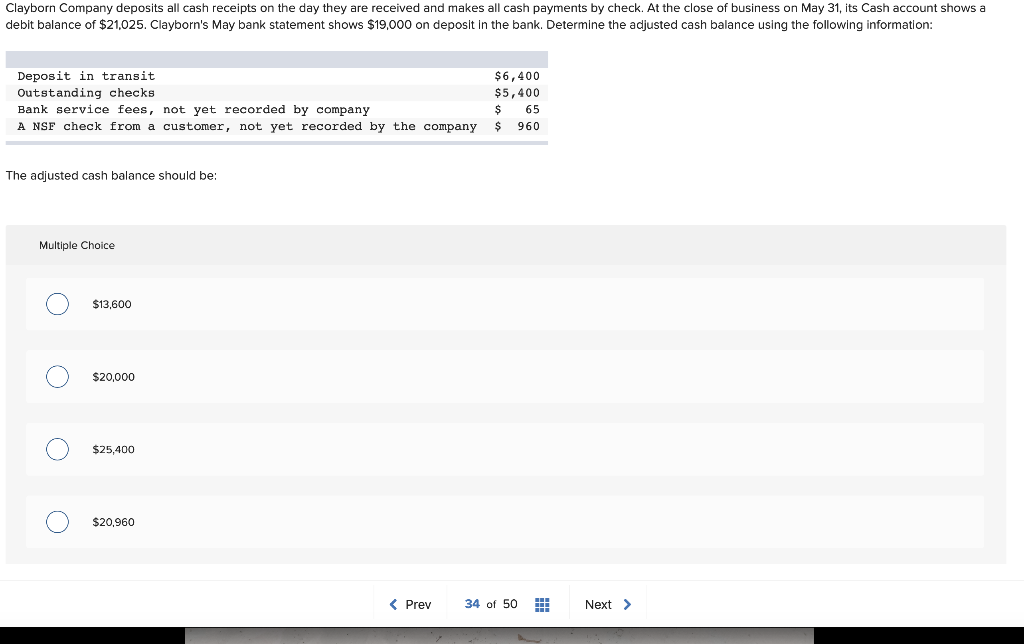

Lender-place insurance? I answr fully your most frequent questions

Or even get homeowner’s insurance, we possibly may must purchase it to you-which will be way more expensive. This is how to eliminate you to definitely.

Providing a mortgage form taking on several judge financial obligation-among that’s up to you to get and keep maintaining homeowner’s insurance rates. Whether your mortgage provides a keen escrow membership, it’s fairly very easy to accomplish that. As to the reasons? Since your insurance fees are part of your typical mortgage repayment; and-as your financing servicer-i spend those people debts for you. But when you don’t possess an enthusiastic escrow account, you only pay the insurance costs oneself.

So what happens if not pay the expenses as well as your insurance carrier cancels your own plan? Or can you imagine the value of your property develops to help you in which your own coverage cannot pay enough to resolve or reconstruct after a flame, violent storm, or any other disasters?

Lender-place insurance (LPI) was possessions insurance coverage that we get on the lender’s behalf when the we should instead: that’s, in the event the homeowner’s coverage lapses or perhaps is canceled-or you payday loans – Illinois do not have adequate exposure. Following we bill your for the prices, which is way more expensive than nearly any rules you should buy your self.

How do you avoid LPI? Continue reading to find out more-and for remedies for the fresh new LPI inquiries, people inquire most frequently.

So why do I wanted homeowner’s insurance?

Basic, to meet your judge responsibility. When you buy property, your mortgage arrangement demands you to definitely purchase and maintain insurance coverage on the your residence.

Second, to protect your property, your loved ones, plus possessions. Can you imagine your residence is insured therefore gets busted or forgotten-such, of the a flame or a tornado. If it goes, their homeowner’s policy handles this new capital one to both you and your bank made of your home. It does you to by paying to displace your own destroyed assets and you can generate solutions-otherwise reconstruct.

But what in case the house is not insured and it becomes heavily damaged otherwise forgotten? You really will not have adequate money on hand to change the of residential property-a lot less to correct or rebuild your home. If that happens, you and your bank loses everything you committed to the house or property. That’s why it’s very essential that the assets be protected from the homeowner’s insurance (possibly named hazard insurance).

What is actually LPI?

LPI is oftentimes titled creditor-placed, force-placed, or equity-safeguards insurance policies. Its an insurance policy that people buy while buy; it talks about your property on the behalf of your own financial. You have to know that people pick LPI only when the audience is obligated to. That is or even replace otherwise replace your homeowners’ insurance coverage policy shortly after they lapses, will get canceled, or does not have any sufficient coverage. Most other grounds we may get LPI is that we simply have no proof you have a recent plan-or we can’t verify that your own coverage provides visibility throughout the a great certain time.

Including, whether your home is inside the a good FEMA-formal flooding zone, you should purchase flood insurance rates. Exactly what without having ton insurance rates? Or imagine if you don’t have sufficient to meet the judge lowest amount wanted to manage your property? When it comes to those cases, their lender might need us to buy ton insurance policies for your possessions.

This type of insurance policy is called lender-placed because your bank has us place it in place to you personally. As well as, LPI covers simply the financial up against assets destroy and losses; it does not security your personal property or whatever responsibility (such as for instance, in the event the neighbors falls in your yard and sues one purchase high priced treatment).

LPI can come from the a higher pricing than homeowner’s insurance policies you order on your own. A primary reason it’s so costly is because it needs to your extremely high risk by guaranteeing possessions in place of an evaluation-and you can as opposed to researching the fresh property’s losings history.